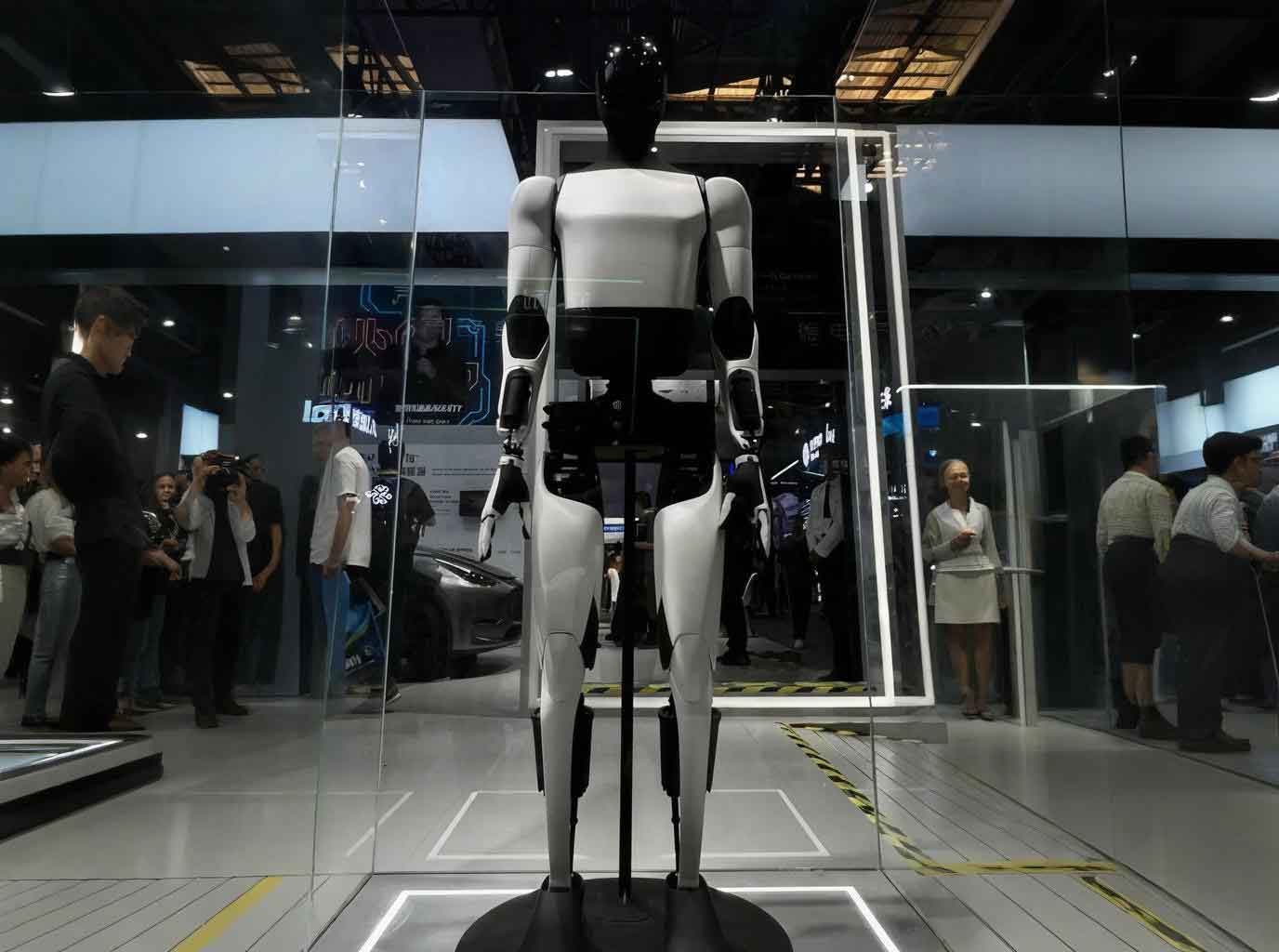

The global landscape of embodied intelligence witnessed a significant milestone with the recent completion of the world’s first half-marathon for humanoid robots. The “Tiangong Ultra” embodied robot clinched victory by crossing the finish line in 2 hours 40 minutes and 42 seconds, drawing international attention to its developer, the Beijing Humanoid Robot Innovation Center Co., Ltd. This event underscores accelerating corporate investments in embodied intelligence technologies, with China’s three major telecom operators now confirming their strategic entries into this burgeoning field.

1. Collective Deployment by Telecom Giants

Telecom behemoths are actively shaping the future of embodied robotics through dedicated initiatives. China Mobile established the China Mobile Embodied Intelligence Industry Innovation Center earlier this year, positioning it as a counterpart to national-level innovation hubs in Shanghai and Beijing. This center targets advancements in robotic capabilities for home environments while developing comprehensive technical frameworks for embodied robots.

Zhao Yongsheng, Technology Management Director at China Mobile’s Smart Home Operation Center, revealed concrete commercialization plans: “Our self-developed quadruped household embodied robot will undergo trial sales in June or July this year. Simultaneously, our newly launched reception-guide embodied robots are already operational in Guangzhou pilot programs.” He emphasized China Mobile’s ambition to become the world’s largest embodied robot operator, leveraging its 686,000+ communication base stations and 1 billion+ mobile customers for market penetration.

China Telecom’s artificial intelligence research institute (TeleAI) is advancing its “AI Flow” framework to coordinate heterogeneous embodied robots across manufacturing ecosystems. As explained by company representatives, this system enables synchronized operations where robotic canines conduct safety inspections, mechanical arms handle precision material transfers, and other specialized embodied robots perform complex assemblies through cloud-edge-device integration.

China Unicom’s IoT platform, Lenovo Gewu, is building core competencies for embodied robots through multi-protocol adaptation, cross-network connectivity, multimodal sensory data fusion, and cloud-edge AI coordination. These capabilities aim to standardize intelligent upgrades across diverse robotic platforms.

2. Expanding Market Trajectory

Government recognition has accelerated the sector’s momentum, with embodied intelligence making its inaugural appearance in China’s 2025 Government Work Report as a prioritized future industry alongside quantum technology and 6G. Market analysis from HeadBrain Research indicates substantial growth, projecting expansion from 418.6 billion yuan in 2023 to 632.8 billion yuan by 2027.

| Year | Market Size |

|---|---|

| 2023 | 418.6 |

| 2027 | 632.8 |

Zhao Yongsheng identifies dual catalysts driving this expansion: “Embodied robots address critical societal challenges like aging populations and labor shortages while enhancing productivity. Concurrently, breakthroughs in multimodal AI models now require physical interfaces to interact with human environments—a role optimally filled by humanoid embodied robots.” This convergence positions embodied robots as essential conduits between digital intelligence and physical-world applications.

3. Commercialization Pathways and Expert Perspectives

Despite optimistic projections, industry players express uncertainties regarding viable monetization models for humanoid embodied robots. Song Xiaofei, Deputy Chairman of the Young Investors Club, contextualizes this challenge: “The embodied robot sector is entering deep-water implementation. Hardware cost optimizations and AI empowerment are shifting the industry from experimental validation toward practical deployment. Major players’ involvement will accelerate technical iterations and scenario adaptations.”

Wang Huajun, Chief Machinery & Defense Analyst at Zhejiang Securities, delineates a phased commercialization roadmap: “Short-term viability hinges on technical validation within vertical applications like logistics sorting and high-risk rescue operations. Medium-to-long-term success requires reconfiguring industrial chains through AI computing leaps and biomimetic material innovations.” He highlights China’s manufacturing advantages in component localization and scenario-specific data accumulation as critical competitive differentiators for embodied robot development.

Industry observers note that telecom operators’ extensive infrastructure—including nationwide 5G networks, distributed computing resources, and massive customer touchpoints—provides unique advantages for scaling embodied robot services. These assets enable real-time data processing for robotic decision-making and create integrated service ecosystems where embodied robots function alongside existing digital offerings. As technical maturation converges with operational scaling, embodied robots are poised to transition from specialized tools to mainstream productivity assets across consumer and industrial domains.