Shenzhen hosted a landmark symposium titled “Embodied Intelligence Ecosystem Empowerment: Shaping the Future Industrial Landscape” at the Shenzhen Stock Exchange on April 10, spotlighting China’s rapid advancements in humanoid robotics technology. The event revealed unprecedented international investor interest, with Ubtech’s Chief Financial Officer Zhang Ju detailing a Wall Street roadshow where meetings were booked solidly from 9 AM to evening for an entire week. “Even Cathie Wood’s ARK Invest had to squeeze in a lunchtime meeting,” Zhang noted, underscoring the intense global capital inflow into China’s embodied intelligence sector.

This investment surge stems from four fundamental value drivers positioning China at the forefront of embodied intelligence innovation. Industry analysts confirm the sector is transitioning from technological validation to pre-industrialization breakout, with embodied robots expected to penetrate diverse commercial applications within 5-10 years.

1. Policy Framework and Capital Commitment

For the first time, “embodied intelligence” entered China’s Government Work Report this year, signaling national strategic priority. Regional governments have responded with concrete action plans: Beijing unveiled the “Beijing Embodied Intelligent Technology Innovation and Industry Cultivation Action Plan (2025-2027)” on February 28, followed by Shenzhen’s “Shenzhen Embodied Intelligent Robot Technology Innovation and Industrial Development Action Plan (2025-2027)” on March 3. The National Artificial Intelligence Investment Fund further solidified support by pledging “patient capital” for long-term, stable funding of core technological breakthroughs. These coordinated policies create fertile ground for embodied robot development, with state-backed capital mitigating early-stage R&D risks.

2. Integrated Industrial Ecosystem

Shenzhen’s unparalleled hardware supply chain exemplifies China’s vertical integration advantage. The city enables rapid local sourcing of critical components—servo motors, sensors, controllers—slashing development costs by 30-40% compared to international counterparts. This clustered efficiency has dramatically boosted domestic substitution rates. Leju Robotics reported its first humanoid embodied robot had just 10% Chinese-made components, while current models achieve 90% localization. The seamless “components-manufacturing-application” industrial chain has accelerated innovation cycles for embodied robots, with prototype-to-production timelines compressed by nearly 50% since 2023.

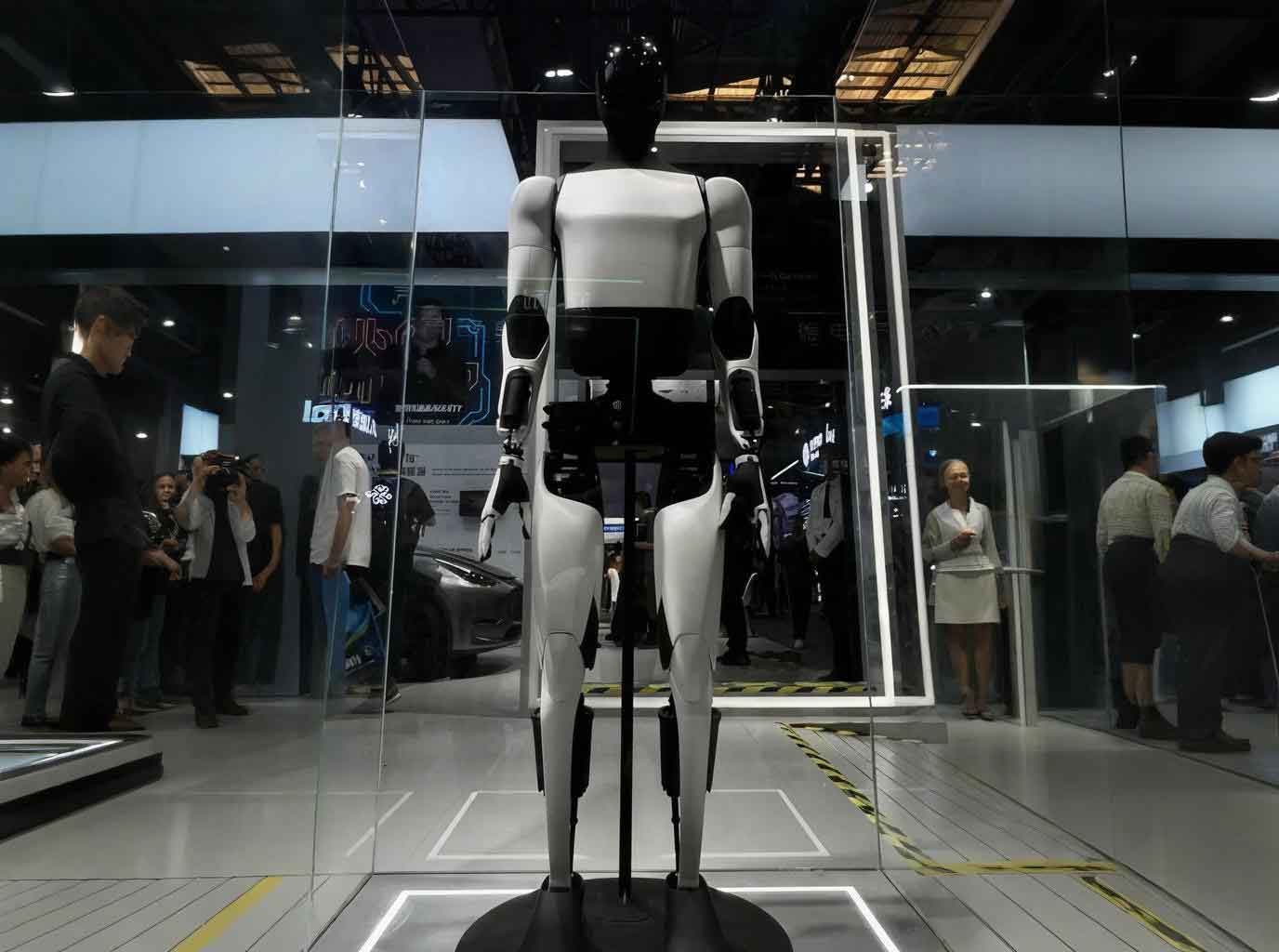

3. Core Technological Breakthroughs

Chinese firms are achieving hardware and software milestones previously dominated by Western companies. Shenzhen Zhongqing Robot Technology has pioneered full-stack R&D capabilities spanning motors, reducers, torque sensors, and communication architectures. Its neural-network gait algorithms enable globally unprecedented natural human-like locomotion in embodied robots. Simultaneously, Jiangsu Leili pushes mechanical frontiers with hollow-cup motors measuring under 8mm diameter and 100,000 RPM speeds, supported by 58 automated production lines ensuring mass-scale precision manufacturing. These innovations overcome historical bottlenecks in dexterity and mobility for embodied robots.

4. Accelerated Commercialization

Dubbed “AI’s ultimate application,” embodied robots demonstrate clear monetization pathways across expanding sectors. Ubtech’s humanoids now supply Tesla’s production facilities, while Zhongqing Robot Technology delivered its first batch of SA01 research-focused bipedal embodied robots within two months of launch. Deployment now spans manufacturing, elderly care, hazardous operations, and education. Industry data indicates embodied robot installations in Chinese factories grew 200% year-on-year in Q1 2025, with service-oriented models entering 10,000+ households. This rapid scenario diversification proves the embodied robot’s economic viability beyond niche applications.

| Technology Domain | Key Advancement | Commercial Impact |

|---|---|---|

| Motion Control | End-to-end neural gait algorithms | Human-like dynamic stability in embodied robots |

| Actuation Systems | 8mm/100k RPM micro-motors | Precision movement for compact embodied robots |

| Manufacturing | 58 automated production lines | Scalable embodied robot assembly |

| Localization | 90% domestic components | Reduced embodied robot production costs |

Despite progress, hurdles persist. High-end chips and sophisticated motion control systems remain partially import-dependent, while scarce high-quality training data impedes AI development. Industry fragmentation also challenges standardization efforts, with 60+ Chinese embodied robot developers pursuing divergent technical routes. “Collaborative frameworks between academia, manufacturers, and data providers are still evolving,” acknowledged a symposium participant.

Global funds increasingly view embodied robots as the next trillion-dollar hardware platform. With “patient capital” commitments exceeding $2 billion and policy-engineered innovation clusters maturing, China’s embodied intelligence sector is positioned to lead the global robotics transition. As component costs decrease 15-20% annually, analysts project embodied robots will achieve price parity with specialized industrial machines by 2028, unlocking mass adoption. The convergence of state support, manufacturing prowess, and accelerating commercial deployments suggests China’s embodied robot revolution is transitioning from laboratory curiosity to economic catalyst.