The humanoid robot sector is witnessing unprecedented growth momentum as research advancements accelerate and global tech giants intensify their strategic deployments, drawing significant investor interest. Wind data reveals that the Wind Humanoid Robot Concept Index surged 3.69% on May 12, marking a cumulative increase of 26.74% since April 9.

Industry analysts assert that humanoid robots represent the optimal embodiment of embodied intelligence, with vast development potential. The year 2025 is projected to mark the explosive starting point for this industry, presenting substantial industrial upgrading opportunities across the humanoid robot value chain.

1. Market Performance and Catalysts

Multiple stocks within the Wind Humanoid Robot Concept Index recorded significant gains on May 12, including Topstar (20% limit-up), Leadec, Efort, and Tongli Tech (all exceeding 10% growth). This bullish sentiment follows several industry developments:

- Unitree Robotics: CEO Wang Xingxing highlighted at the 6th Shanghai Innovation and Entrepreneurship Youth 50 Forum that humanoid robot enterprises are thriving due to market enthusiasm and supportive national policies. “Many companies, including Unitree, are overwhelmed with orders,” Wang stated, emphasizing unprecedented demand and robust industry-wide growth.

- Huawei-UBTech Partnership: On May 12, Huawei and UBTech signed a comprehensive cooperation agreement to jointly innovate in embodied intelligence and humanoid robotics. Huawei will leverage its Ascend, Kunpeng, cloud computing, and large-model technologies to enhance UBTech’s full-stack humanoid robot capabilities. The collaboration focuses on accelerating industrial and household applications through an Embodied Intelligence Innovation Center and developing “humanoid robot + smart factory” solutions, including bipedal and wheeled domestic service humanoid robots.

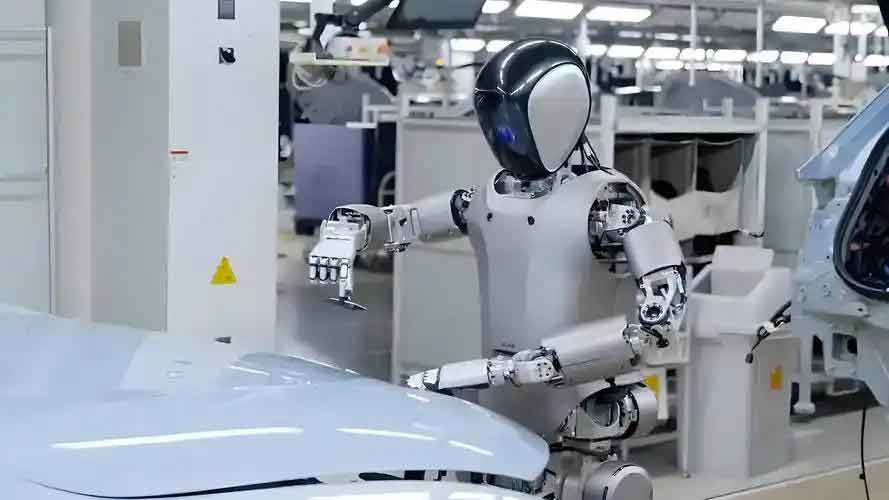

- Midea Group’s Industrial Deployment: The self-developed humanoid robot “MIRO” has commenced operational duties at Midea’s washing machine factory in Jingzhou, Hubei. Standing 1.9 meters tall and weighing 68 kilograms, MIRO features 16 degrees of freedom, 6 active joints, and six-dimensional force sensors. Its initial responsibilities include facility inspection, data collection, and equipment maintenance.

2. Financial Performance Highlights

First-quarter 2025 financial results demonstrate robust growth across the humanoid robot supply chain. Among 109 companies listed in the Wind Humanoid Robot Concept Index, 77 (70.64%) reported revenue growth. Notable performers include:

| Company | Revenue (CNY) | YoY Growth | Net Profit (CNY) | YoY Growth |

|---|---|---|---|---|

| Inovance Technology | 8.98 billion | 38.28% | 1.32 billion | 63.08% |

| Shuanglin Group | 1.29 billion | 20.97% | 159 million | 105.49% |

| Allwinner Technology | 620 million | 51.36% | 92 million | 86.51% |

Li Hang, Chief Analyst of Power Equipment and New Energy at Guohai Securities, noted: “Amid electrification and smartization trends, domestic and international humanoid robot products continue to iterate, creating pivotal ‘0 to 1’ investment opportunities. Mass production and commercial adoption of humanoid robots are accelerating, potentially heralding the industry’s ‘ChatGPT moment’.”

3. Investment Outlook and Market Projections

The humanoid robot industry is transitioning from singular performance breakthroughs to complex real-world applications, with development pathways becoming increasingly clear. Key market forecasts include:

- Market Scale: Qiu Shiliang, Co-Director of Zheshang Securities Research Institute, projects combined demand of approximately 2.1 million humanoid robots in Chinese and American manufacturing and housekeeping sectors by 2030, representing a market value of CNY 314.6 billion.

- Core Components: Dexterous hands, planetary roller screws, and reducers constitute critical humanoid robot components, forecasted to reach CNY 102.2 billion by 2030.

Zou Runfang, Assistant General Manager and Director of AVIC Securities Research Institute, emphasized: “2025 marks the inaugural year of mass production for humanoid robots. Continuous software enhancements and clearer capacity planning from global manufacturers indicate an industry in vigorous expansion. Investment opportunities across the humanoid robot supply chain should be prioritized during this inflection point.”

Lu Pei, Chief Machinery Analyst at China Galaxy Securities, identified three enterprise categories warranting investor focus:

- High-Certainty Players: Companies with confirmed orders, business/investment collaborations, product milestones, or capacity expansions poised to benefit from scaled deliveries.

- Core Component Suppliers: Entities controlling high-value, irreplaceable segments of humanoid robot manufacturing.

- Emerging Innovators: Firms driving marginal advancements in dexterous hands, sensors, motion control systems (“cerebellum”), and embodied AI models.

The convergence of technological breakthroughs, industrial applications, and policy support continues to solidify the humanoid robot sector’s position as a transformative force in global manufacturing and service economies.