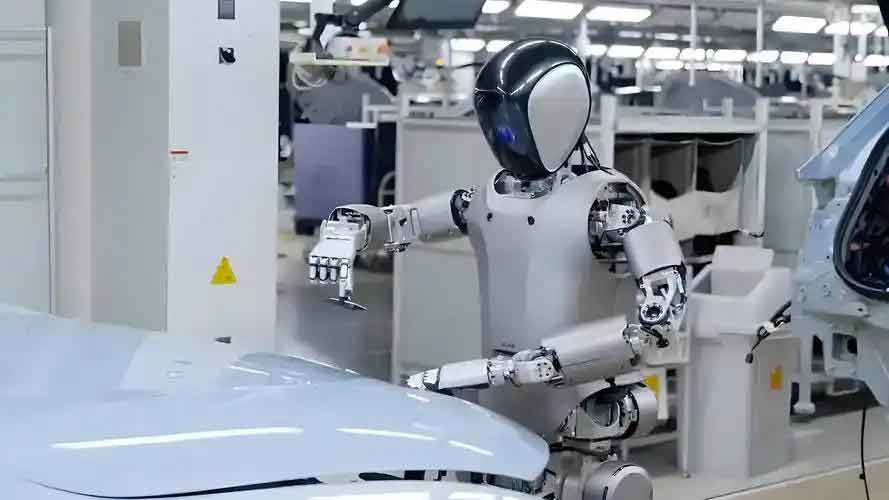

In a significant milestone for the robotics industry, Shanghai Zhiyuan New Creation Technology Co., Ltd. (“Zhiyuan”) announced on March 10 that its cumulative production of general-purpose embodied humanoid robots has exceeded 1,000 units. The company is also set to host the “1+4 Zhiyuan Qiyuan Large Model” and Lingxi X2 Embodied Intelligence Humanoid Robot offline launch event in Zhuhai on March 14. These developments have sparked widespread attention across industries, fueling expectations that humanoid robots are nearing a critical mass production node.

Zhang Xinyuan, Executive General Manager of Beijing Kefangde Technology Development Co., Ltd., told Securities Daily that Zhiyuan’s successful rollout of 1,000 robots signifies that the company has achieved scale production capabilities in technological R&D, manufacturing processes, and supply chain management. This milestone marks a breakthrough for humanoid robots transitioning from the laboratory stage to commercial application, Zhang noted. “This news will boost confidence across the robotics industry, attracting more enterprises and capital into the humanoid robot sector and accelerating industrial technological innovation and upgrading,” he added.

Technical Breakthroughs and Policy Momentum

Technologically, domestic humanoid robot developers have continued to make significant strides. In January, Zhiyuan held a delivery ceremony for its Lingxi X1 humanoid robots in Changsha, successfully completing batch deliveries of related products. On March 10, the company officially launched the embodied intelligence large model GO-1, empowering robots to make autonomous decisions in complex environments. This model enhances robots’ adaptability and operational efficiency, representing a key step toward realizing intelligent autonomy in humanoid machines.

Meanwhile, major tech companies are ramping up their efforts in the humanoid robot space. Xiaomi Corporation has recently disclosed a series of robot-related patents and initiated intensive recruitment for relevant positions, with plans to showcase its latest advancements and gradually implement production line applications between March and April. XPeng Robotics has already deployed its robots in a Guangzhou factory and aims to achieve L3 mass production by 2026. Other players such as Hangzhou Unitree Technology Co., Ltd., Shenzhen UBTECH Robotics Corp. Ltd., and Shenzhen Zhongqing Robotics Technology Co., Ltd. have also unveiled new developments in their robot products, reflecting a collective push toward technological maturity and commercialization.

Supporting these technological advancements is a robust policy framework. In March, “embodied intelligence” was included in the Government Work Report for the first time, highlighting the Chinese government’s strategic emphasis on the field. Statistics show that more than 20 cities in China have explicitly proposed plans to develop embodied intelligence. Shenzhen alone is home to 51,100 robot-related enterprises, with an industrial chain output value exceeding 170 billion yuan. This policy-driven environment has created a favorable ecosystem for humanoid robot manufacturers and their supply chains, accelerating the pace of mass production.

Analytical reports further underscore the growing momentum. A research note by Kaiyuan Securities states that both domestic and international humanoid robot mass production is expected to exceed expectations between 2025 and 2026. Wanlian Securities echoes this optimism, emphasizing that 2025 could see dual drivers of technological breakthroughs and mass production for the humanoid robot industry. The open-source ecosystem and generalization capabilities of Zhiyuan’s GO-1 large model are poised to inject new momentum into the sector, according to the report.

Listed Companies’ Deep Involvement in the Supply Chain

As the humanoid robot industry gears up for mass production, supply chain enterprises are positioned to be the first beneficiaries. A recent robotics industry report by Goldman Sachs predicts that the global humanoid robot market could reach $38 billion by 2035, with supply chain companies standing to gain significantly. Several A-share listed companies have already established first-mover advantages in the core supply chain of humanoid robots, securing key positions in the emerging industry.

Yuhuan CNC Machine Tool Co., Ltd. has forged partnerships with reducers manufacturers in the humanoid robot sector. The company’s broaching machine series products have been delivered for processing components of planetary reducers, demonstrating its capability to contribute to critical mechanical parts production.

Lens Technology, a core supplier to Zhiyuan, has deeply participated in the production, assembly, and testing of key components for the Lingxi X1 robot, including joint modules, DCU controllers, and grippers. The company offers one-stop vertical integration services from design to mass production and has partnered with leading domestic and North American humanoid robot companies. It has established specialized teams to develop robot joints, dexterous hands, torso and head casings, expression masks, and complete machine assembly, highlighting its comprehensive supply chain capabilities.

Other listed companies have also disclosed their humanoid robot initiatives through investor interactions. For instance, iSoftStone Information Technology (Group) Co., Ltd.’s subsidiary iSoftStone Tianqing Robotics launched its first bipedal robot for interaction and education, the Tianhe C1, in January. Ningbo Junpu Intelligent Manufacturing Co., Ltd. has sent small batches of humanoid robot products for sampling and testing, while Ningbo Keli Sensing Technology Co., Ltd. has established a robot business division and R&D team to proactively engage with various robot clients in the market.

Implications for the Industry and Supply Chain Growth

The mass production breakthrough and technological innovations in humanoid robots not only set a benchmark for China’s domestic industry but also open up growth opportunities for A-share supply chain companies. Zhang Xinyuan emphasized that mass production of humanoid robots will directly drive order growth for 零部件 (components) suppliers. Additionally, supply chain enterprises may engage in deeper technical collaboration with leading robot manufacturers to jointly develop higher-performance and lower-cost components, driving supply chain technology upgrades.

This symbiotic relationship between manufacturers and suppliers is crucial for the industry’s long-term development. As humanoid robots become more sophisticated, the demand for advanced components such as precision reducers, sensors, and intelligent control systems will surge. Supply chain companies that can adapt to technological requirements and scale production will likely secure larger market shares, while those lagging in innovation may face challenges.

Conclusion: A New Era for Humanoid Robotics

The recent developments at Zhiyuan and other industry players signal that humanoid robots are on the cusp of transitioning from niche R&D to mainstream production. With technological advancements, policy support, and active participation from supply chain enterprises, the industry is poised for rapid growth in the coming years.

For investors and industry observers, the focus now shifts to how supply chain companies will leverage this momentum to enhance their capabilities and capture market opportunities. As Goldman Sachs’ report suggests, the humanoid robot market’s exponential growth in the coming decade will likely reshape industries ranging from manufacturing to services, with supply chain resilience and innovation emerging as key differentiators.

In this evolving landscape, China’s humanoid robot industry stands at the forefront, driven by a combination of technical prowess, policy foresight, and a robust industrial ecosystem. As mass production becomes a reality, the ripple effects on employment, technology, and global trade will be far-reaching, marking the dawn of a new era in intelligent automation.