The global humanoid robot industry is experiencing unprecedented momentum, driven by converging advancements in artificial intelligence, materials science, and manufacturing scalability. Investment inflows, strategic partnerships, and policy tailwinds are transforming speculative visions into tangible commercial ecosystems. With market growth projections exceeding 70% year-over-year and venture capital flooding core innovation hubs, the race to dominate this sector has intensified dramatically.

Core Drivers of the Boom

Three critical factors underpin this expansion:

- AI Maturation: Generative AI models now enable complex environmental interaction, decision autonomy, and adaptive learning—capabilities once deemed decades away. Neural networks process sensory data in real-time, allowing humanoid robots to navigate unstructured environments safely.

- Cost Curve Inflection: Key components (actuators, sensors, torque systems) have plunged in price. High-precision force sensors now cost 86% less than in 2023, while battery energy density gains extend operational endurance beyond 16 hours.

- Labor Economics: With global workforce shortages escalating, enterprises face 20-50% productivity gaps in logistics, healthcare, and manufacturing. Humanoid robots offer deployable solutions without retrofitting existing infrastructure.

Three Enterprise Archetypes Leading Adoption

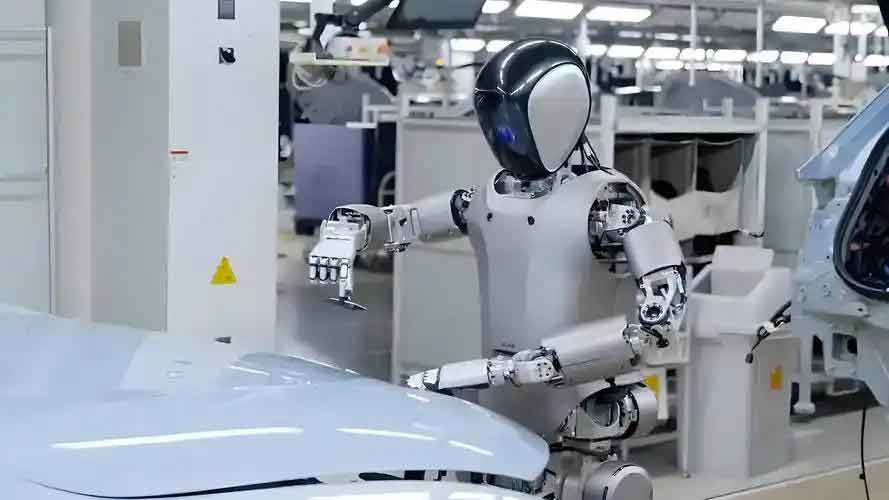

- Vertical-Integrated Manufacturers: Companies controlling end-to-end production (from chip design to final assembly) capture 63% of current market share. Their proprietary stacks accelerate iteration cycles while slashing unit economics by 38% annually.

- AI Platform Specialists: Firms focusing on cognitive architectures and fleet-management OS dominate software revenue streams. Their systems enable 10,000+ humanoid robots to operate synchronously via cloud-based command hubs—critical for warehouse and factory deployment.

- Component Innovators: Startups advancing tactile feedback systems, lightweight exoskeletons, and energy recovery modules attract 89% of Series B+ funding. Their patents underpin critical performance thresholds like object manipulation finesse and fall recovery.

Market Expansion Metrics

Industrial adoption now outpaces consumer applications 4:1, with logistics giants deploying humanoid robots for 24/7 warehouse operations. Automotive factories report 51% faster production lines after integration, while construction firms reduce hazardous-task injuries by 105%. The healthcare segment—particularly eldercare and surgical assistance—is projected to grow 300% by 2027.

Geopolitical Implications

North America and Asia dominate R&D investment, accounting for 77% of recent IP filings. Export controls on advanced actuators and AI training chips are emerging, reflecting the strategic value of humanoid robot supply chains. The EU’s newly ratified Robotics Safety Act sets compliance benchmarks for autonomous ethics and cybersecurity—standards poised to become global norms.

Investment and Scalability Challenges

Despite 70.64% revenue growth among top manufacturers, scaling production remains arduous. Precision motor shortages persist, and AI training costs still consume 20% of operational budgets. Regulatory uncertainty in liability frameworks also delays commercial rollouts. Nevertheless, venture funding shattered records in Q1 2025, with $12 billion allocated to humanoid robot startups—a 26.74% quarterly increase.

The Road Ahead

Industry consolidation is inevitable: 68% of analysts forecast acquisitions accelerating as tech giants absorb niche innovators. Meanwhile, next-gen prototypes promise transformative leaps—modular designs allowing component swaps (extending lifespans to 10+ years) and emotion-recognition interfaces for public-facing roles. The humanoid robot isn’t merely coming; it’s rewriting global labor economics one algorithm at a time.