The humanoid robot industry represents a pivotal frontier in cultivating and developing new quality productive forces, serving as a new track for future industries and a new engine for economic growth. This analysis explores the application scenarios, ecosystem shortcomings, and future directions of the humanoid robot industry based on the triadic ecological system framework of “Driving Force–Constraint Force–Guiding Force.” Research indicates that the application scenarios for humanoid robots evolve along the logic of “demonstration–pilot–diffusion,” progressively moving from feasibility showcases to functional applications. Currently, the industry faces five major ecosystem shortcomings: cost, technology, industrial chain synergy, capital chain, and industry standards, which collectively form critical barriers from prototype breakthroughs to scaled deployment. To transform application scenarios into widespread, large-scale adoption, the future necessitates breakthroughs in these existing constraints through policy guidance, expansion of application scenarios, optimization of the technology system, upgrading of industrial organization, reduction of costs across the entire industrial chain, and the establishment of a robust governance and standards framework to propel the high-quality development of the humanoid robot industry.

Application Scenarios of the Humanoid Robot Industry: The Driving Force

The breakthrough of technology does not equate to industrial success. For a complex future industry like humanoid robotics, the key to moving beyond the laboratory is not the refinement of a single algorithm, material, or hardware component, but whether these innovations can be embedded into real-world scenarios and generate positive feedback. The ultimate significance of a humanoid robot lies not merely in its ability to “walk” or “dance,” but in being genuinely “useful” through actual use. Therefore, the true threshold for industrialization is not building a prototype, but identifying suitable application scenarios. In the era of the digital economy, the focal point of competition in the humanoid robot industry is shifting from technology to ecosystem, with the driving force of this ecosystem being the application scenario.

The application of humanoid robots exhibits both regularity and pervasiveness. On one hand, the theory of innovation diffusion suggests that the adoption of humanoid robots follows an S-curve trajectory of “slow start–rapid diffusion–stabilization.” This curve mirrors the adoption path of the automobile industry in the early 20th century. Growth is initially slow, accelerating rapidly after a critical tipping point is reached. This tipping point is triggered when rising technical credibility and a falling cost curve form a closed-loop with real scenarios. As technology generates data and refines algorithms within actual applications, costs decrease, creating a virtuous cycle of “technology–scenario–feedback–re-innovation.” It is the continuous operation of this closed-loop that enables the industry to transition from supply-driven to demand-pulled growth, catalyzing accelerated diffusion. On the other hand, the application boundaries of humanoid robots are continuously expanding. This pervasiveness stems not from the叠加of tasks, but from their general-purpose nature and ecological adaptability. Humanoid robots represent a leap from tool-based robotics to intelligent agents. Their value lies in maintaining functional stability and decision-making adaptability in complex, non-structured environments, making them a universal intelligent interface within new quality productive force systems.

Current Application Scenarios and Their Evolution

The commercialization of humanoid robots is undergoing a transition from feasibility demonstration to functional application. This process is shaped by the combined effect of technological maturity and market viability. From the supply side, technology determines what a humanoid robot *can* do; from the demand side, the scenario determines where it *will be* used.

In the nascent stage of China’s humanoid robot industry, these robots primarily served a “demonstrative” role. Early commercial scenarios included education, research, entertainment performances, and commercial services. Humanoid robots like Ubtech’s Walker series and the panda robot “Youyou” were widely used in theme parks and exhibitions, performing high-precision actions in complex environments. These high-exposure scenarios not only validated technical feasibility but also cultivated public perception of humanoid robots as “capable and approachable,” laying a social认知foundation for their entry into industrial and public service domains.

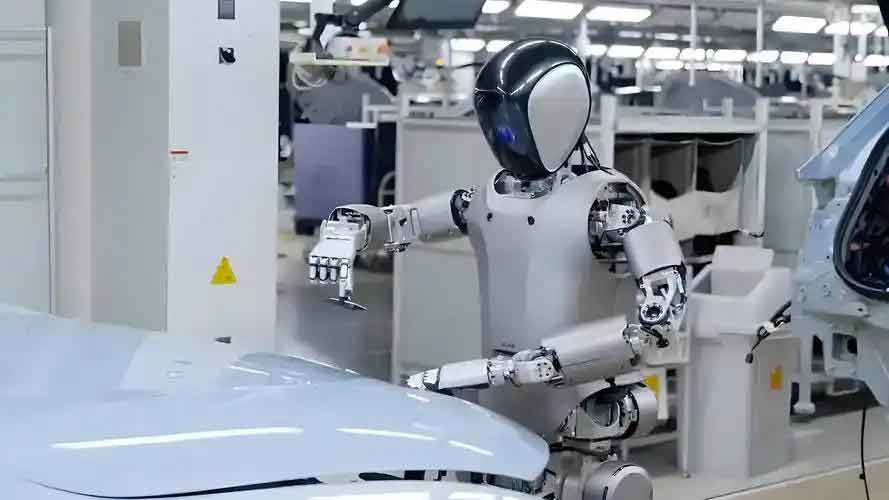

Following this, humanoid robots entered a phase of application guided by technical performance and economic feasibility. The industrial manufacturing sector, particularly automotive, became a core area for early commercialization. Since late 2023, humanoid robots have gradually moved from lab demos to pilot programs on production lines. Humanoids like Ubtech’s Walker S and Zhiyuan Robotics’远征A1 have been tested in automotive and 3C manufacturing. These tasks, characterized by clear节拍, high repetitiveness, and semi-structured environments, mark the preliminary leap for humanoid robots from “demonstrating feasibility” to “proving effectiveness.” By 2024, the focus shifted further from effectiveness to stable operation at an acceptable cost. This stage signifies the transformation of humanoid robots from technical prototypes to production factors, becoming a new variable in enhancing the efficiency of flexible manufacturing systems.

After industrial pilots validate technical feasibility, social demand becomes a new driving force for the diffusion of application scenarios. Unlike manufacturing, the service sector has long been constrained by high-touch, highly uncertain, and difficult-to-standardize tasks, leading to high labor turnover and fluctuating service quality. This presents an opportunity for humanoid robots to functionally complement “human labor短板.” Demand is concentrated in retail, healthcare, and elderly care. In retail, tasks like guided tours, inquiries, and inventory checks are流程清晰. In healthcare and elderly care, humanoid robots can assist with both physical-procedural tasks (e.g., moving patients, rehabilitation exercises) and cognitive-emotional tasks (e.g., medication reminders, companionship), optimizing service workflows. Furthermore, Dangerous, Dirty, and Dull (3D) environments—such as mining, disaster rescue, and nuclear facility maintenance—are becoming high-potential demand scenarios where users are more willing to pay a premium for risk-resistant and adaptive robots.

The fusion of scenarios marks the transition of humanoid robots from production factors to social participants. In educational settings, they act as intelligent tutors and emotional intermediaries. In家庭scenarios, they integrate household execution with emotional interaction. The essence of these scenarios is a “social feedback” system where interaction data feeds back to optimize algorithms. The application of humanoid robots is no longer solely dependent on hardware performance but is entering a stage of scenario adaptability—those that can embed themselves more naturally into human life will have higher user stickiness and scalability potential.

Trends and Bottlenecks in Scenario Development

In the long term, the potential scale of humanoid robot applications is significant. Forecasts suggest that if humanoid robots could replace a portion of labor in industrial and service sectors, their penetration rate in a stable stage could reach approximately 0.7 units per household. Service, domestic, and industrial applications are projected to account for 65%, 32%, and 3% of the final application mix, respectively, indicating their evolution into a new type of universal terminal.

However, significant gaps remain before large-scale commercialization. Major bottlenecks include: 1) Hollowing of Application Scenarios: Technological evolution outpaces demand growth, creating a disconnect between demonstrative achievements and practical use. 2) Limited Application Space: Efficiency in industrial environments is only 30-40% of human levels, and functionality in diverse domestic settings remains limited. 3) Unclear Business Models: Profit paths are not well-defined, with high costs and long payback periods undermining traditional sales models. 4) Dual Constraints of Scenario Adaptation and Deployment Cost: High unit costs and algorithmic training expenses exceed the承受能力of most enterprises, while reliability in complex tasks is insufficient for industrial demands.

In summary, the humanoid robot industry is at a critical juncture transitioning from technology to product and from product to ecosystem. The realization and breakthrough of the driving force of application scenarios depend not only on product iteration but also on the reconstruction of the ecosystem—only when humanoid robots can exist within both economic and social logic can they achieve true scaled commercialization.

Ecosystem Shortcomings of the Humanoid Robot Industry: The Constraint Force

The global humanoid robot industry is at a critical node transitioning from single-point technological breakthroughs to confronting ecological constraints. The真正binding factors limiting its commercial落地are not engineering challenges but systemic ecosystem shortcomings. As illustrated in the analysis below, constraints related to standards & regulations, mass production ramp-up, manufacturing costs, financing capability, scenario identification, and industrial talent pose the most significant barriers.

| Ecosystem Shortcoming | Primary Manifestations | Root Causes & Systemic Impact |

|---|---|---|

| 1. Cost Shortcoming | High unit cost ($$C_{unit}$$); Limited cost-reduction paths. | Lack of scale economies; High customization prevents modularity; Supply concentration for core components; High software (AI training) costs. |

| 2. Technology Shortcoming | Performance bottlenecks in core components; System integration complexity; Divergent technical pathways. | Immature, non-standardized key components (actuators, drives); High coupling between perception, decision, and control; Lack of consensus on optimal工程morphology (通用vs.专用). |

| 3. Industrial Chain Synergy Shortcome | Upstream: Available but ineffective supply. Midstream: Many players but weak integration能力. Downstream: Broad scenarios but weak牵引. | Formally complete chain but functionally disjointed; Lack of unified platforms and verification loops; Absence of scene co-creation mechanisms between supply and demand. |

| 4. Capital Chain Shortcoming | Volatile & uneven financing; Funding断层at industrialization stage; Systemic周期mismatch. | Capital偏向narrative-driven整机firms; VC/PE exit cycles (3-7 years) mismatch with technology maturation cycles (10+ years); Amplifies other shortcomings through chain reaction. |

| 5. Industry Standards Shortcoming | Missing基础technical standards (interfaces); Lagging data & scenario rules; Lack of international governance voice. | Prevents modular协同and scaled manufacturing; Creates “data silos” hindering AI generalization; Forms institutional pressure in global competition. |

The cost shortcoming is the most direct barrier. The high unit cost $$C_{unit}$$ can be modeled as a function of hardware cost $$C_{hw}$$, software/R&D cost $$C_{sw}$$, and a scaling factor $$k$$ that is inversely related to production volume $$Q$$:

$$C_{unit} = (C_{hw} + C_{sw}) \cdot k(Q), \quad \text{where } \frac{dk}{dQ} < 0$$

The learning curve effect suggests that cost decreases with cumulative production: $$C_n = C_1 \cdot n^{-b}$$, where $$C_n$$ is the cost of the $$n^{th}$$ unit, $$C_1$$ is the cost of the first unit, and $$b$$ is the learning rate. However, the current low volume and high customization prevent the industry from moving down this curve efficiently.

The technology shortcoming is fundamentally about integration. The reliability $$R_{system}$$ of a humanoid robot is a product of the reliability of its $$N$$ highly coupled subsystems:

$$R_{system} = \prod_{i=1}^{N} R_i$$

A slight drop in the reliability of any single component (e.g., an actuator with $$R_i = 0.99$$) is multiplied across the system, making it challenging to achieve the high $$R_{system}$$ required for continuous, untended operation in real-world settings.

The capital chain shortcoming creates a “valley of death” between prototype and product. The required investment $$I(t)$$ grows exponentially during the industrialization phase, while revenue $$R(t)$$ remains near zero. The funding gap $$G$$ at time $$T$$ is:

$$G(T) = \int_{0}^{T} I(t) \,dt – \int_{0}^{T} R(t) \,dt$$

Traditional venture capital, seeking returns within a short horizon $$[0, T_{exit}]$$ where $$T_{exit} < T_{maturation}$$, is structurally ill-suited to bridge this gap, leading to the funding断层observed in the industry.

Future Directions for the Humanoid Robot Industry: The Guiding Force

The future competitive landscape of the humanoid robot industry will be determined not merely by the speed of innovation, but by a profound synergy spanning application scenarios, the industrial ecosystem, and institutional systems. Breaking through the aforementioned constraint forces requires coordinated action across multiple dimensions, shaping the guiding force for the industry’s evolution.

| Arena of Change | Core Transition | Key Mechanisms & Objectives |

|---|---|---|

| 1. Policy Supply | From financial subsidies to standardized, synergistic, and ecological governance. | Providing institutional public goods (standards, interfaces); Fostering regional innovation networks; Adopting holistic ecosystem governance to manage complexity and externalities. |

| 2. Application Scenarios | From demonstration/pilot to replicable deployment. | Public demonstration projects as testbeds; “Use-to-Research-to-Production” positive feedback loops; Servitization business models (RaaS); Building public trust and social acceptance. |

| 3. Technology System | From fragmentation to open-source, modular, and shared foundational platforms. | Open-source frameworks to lower innovation barriers and prevent duplication; Modular design for flexible configuration and competition; Shared technical底座(e.g., OS, control frameworks) for economies of scale in R&D. |

| 4. Industrial Organization | From linear chains to networked ecosystems. | Deepened industry-university-research collaboration; Multi-node, platform-based enterprise协作; Reconfiguration of knowledge, technology, and value chains into协同networks. |

| 5. Cost Structure | From local cost reduction to whole-industry-chain cost compression. | Material innovation (lightweight, high-strength); Manufacturing process optimization (automation, modularization); Technology integration using AI to replace hardware堆叠, enabling marginal cost递减. |

| 6. Governance System | From product regulation to健全standards体系and enhanced international governance voice. | Establishing full-lifecycle standards covering safety, ethics, and data; Implementing跨部门synergistic regulation; Actively participating in and shaping international rules and standards. |

The future cost compression will be systemic. The target unit cost $$C_{target}$$ for mass adoption requires advances across the chain:

$$C_{target} = f(C_{materials}^{new}, \eta_{manufacturing}, \alpha_{AI})$$

Where $$C_{materials}^{new}$$ represents the cost of new materials, $$\eta_{manufacturing} > 1$$ is the efficiency multiplier from optimized processes, and $$\alpha_{AI}$$ is the cost-reduction factor from AI integration (where $$\alpha_{AI} < 1$$, as software capabilities reduce reliance on expensive hardware). The industry’s trajectory is towards making $$\alpha_{AI}$$ the dominant driver of marginal cost reduction.

In conclusion, the humanoid robot is evolving from a sector-specific product into a全局性future industry. Within this process, the triadic system of scenario-driven demand, ecosystem synergy, and institutional support will redefine the future competitive格局. Technology落地must be embedded in real scenarios; scenario expansion depends on a healthy industrial ecosystem; and ecosystem stability requires policy and institutional underpinnings. The true ceiling for the humanoid robot industry is not set by a breakthrough in any single link, but by the ability to achieve synergy and self-consistency at the systemic level. Therefore, cultivating the humanoid robot industry requires not only a sense of urgency but also strategic patience and a holistic vision.